- Policy Analysis

- PolicyWatch 4227

Syria’s Pipeline Dream Meets Hard Realities

Jun 10, 2026

Also available in

About the Authors

Brief Analysis

Asian market realities and the ongoing risks to energy investments inside Syria may put a damper on any large-scale infrastructure plans, though Damascus can better its prospects through further stabilization and reform efforts.

Washington is abuzz with talk of Syria as the next alternative to the Strait of Hormuz, or at least part of one. As tensions with Iran continue over reopening the waterway, policymakers and investors are searching for ways to reduce dependence on one of the world’s most vulnerable maritime chokepoints, which carried roughly 20-25 percent of the global oil and natural gas trade before the war.

Following the December 2024 collapse of the Assad regime, President Trump’s decision to engage Syria’s new leaders has revived interest in the country’s long-neglected role as a regional energy transit state. Supporters envision pipelines carrying Iraqi and Gulf oil to Mediterranean ports, gas flowing from Qatar to Europe, and infrastructure linking the Persian Gulf, East Mediterranean, Black Sea, and Caucasus. In their view, such projects would diversify global energy routes, strengthen America’s allies in Europe, and reduce Iran’s ability to manipulate energy markets during any future crises.

Yet while these proposals correctly highlight Syria’s strategic geography, they largely ignore a less attractive reality: pipelines have repeatedly made the country a target of political conflict, military confrontation, and sabotage. This history suggests that pipelines crossing Syrian territory are not merely economic assets—they are also strategic vulnerabilities. This is particularly true for proposals to revive the Kirkuk-Baniyas oil pipeline and construct a Qatar-Turkey gas pipeline. Both would traverse vast stretches of sparsely populated territory where Islamic State remnants and Iran-backed Shia militias remain active. More fundamentally, many of these plans overlook a basic commercial reality: the largest and fastest-growing markets for Gulf energy remain in Asia, not Europe, limiting Syria’s attractiveness as a major export corridor for most Gulf producers.

A Century of Pipelines and Instability

Regional pipelines have played a surprisingly consequential role in Syria’s political history from the beginning. The U.S.-backed Trans-Arabian Pipeline (Tapline), built to transport Saudi crude oil to the Mediterranean, contributed to Syria’s first of many political coups. After the state achieved independence in 1946, President Shukri al-Quwatli resisted American pressure to approve Tapline’s crossing of the Golan Heights, viewing it as an infringement on Syrian sovereignty. In March 1949, army chief Husni al-Zaim overthrew Quwatli and quickly approved Tapline—only to be overthrown himself months later as Syria devolved into one of the world’s most unstable countries.

Syrian pipeline routes remained vulnerable when regional conflicts erupted in subsequent decades. During the 1956 Suez Crisis, Israeli forces targeted pumping stations along the Kirkuk-Baniyas pipeline. And in 1982, President Hafiz al-Assad shut down the pipe after aligning with Tehran against Saddam Hussein in the Iran-Iraq War. Later, this route briefly returned to prominence following a secret arrangement between Bashar al-Assad and Saddam, enabling Iraqi oil to once again flow through Syria despite UN sanctions on Baghdad. Yet U.S. forces struck the pipeline’s infrastructure during the 2003 invasion of Iraq, effectively ending operations.

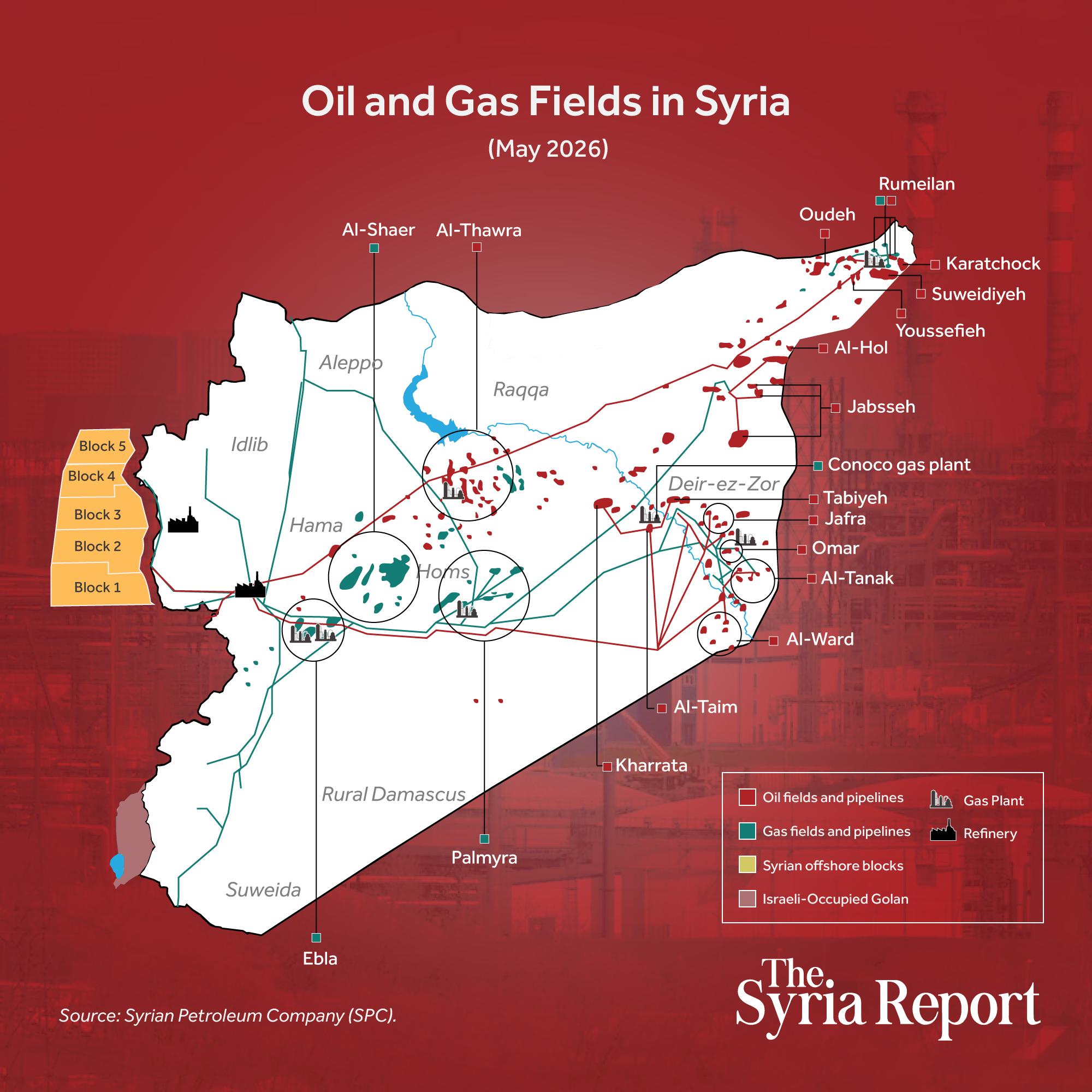

Syria’s civil war destroyed much of what remained. Beginning in 2011, the Islamic State and other armed groups systematically targeted the country’s oil and gas infrastructure. Pipelines, pumping stations, and export facilities became military objectives, sources of revenue, and symbols of state authority. By the time the regime collapsed in 2024, much of Syria’s energy transportation network had been damaged, looted, or rendered inoperable.

The lesson is straightforward: pipelines crossing Syria have rarely been insulated from local or regional crises. More often, they have become casualties of political and military struggles.

Limitations of the Post-Assad Pipeline Revival

Despite this history, Syria’s new government has generated enthusiasm for reviving regional energy projects. Several important initiatives are already operating:

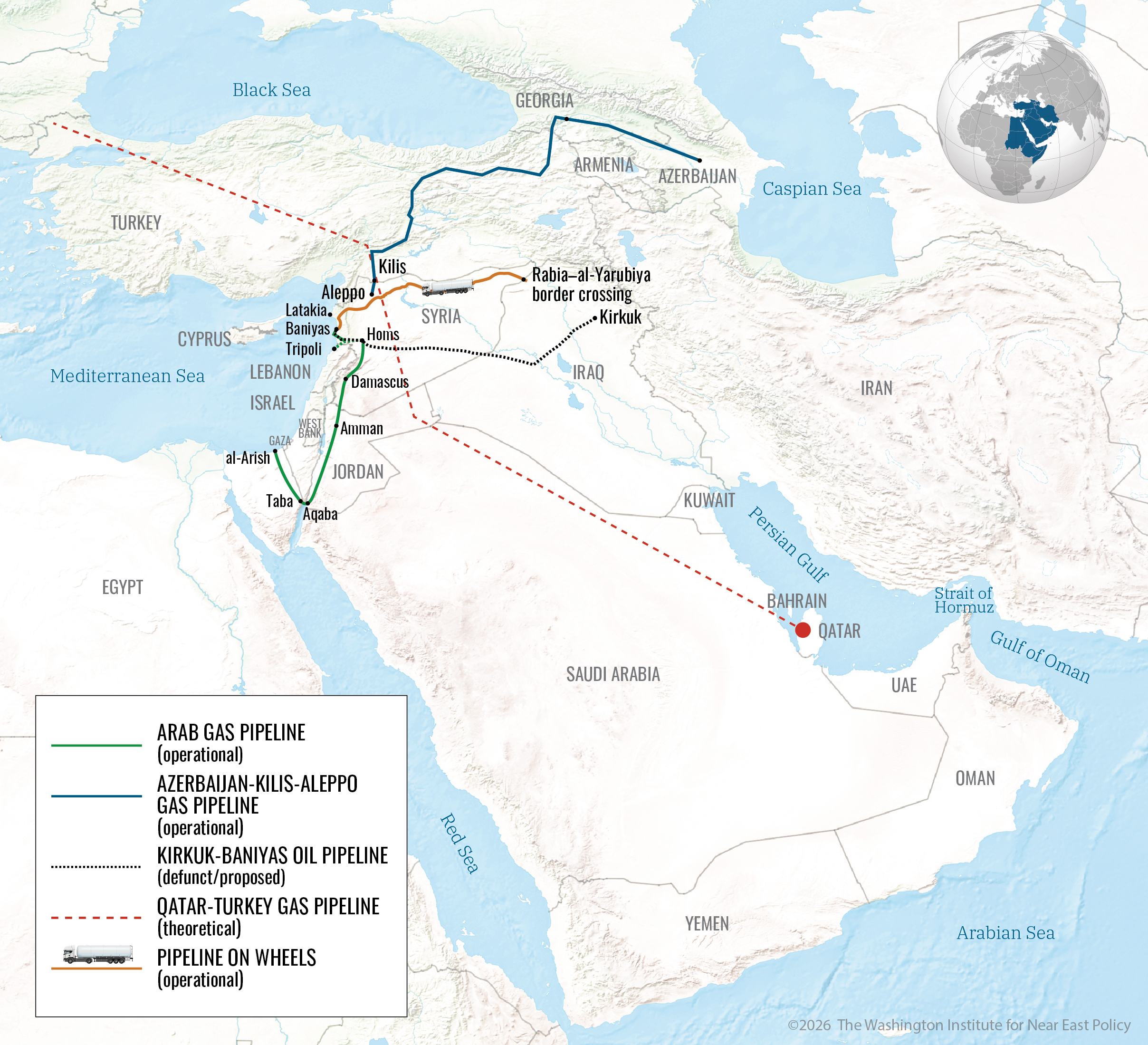

- The Arab Gas Pipeline is once again carrying supplies northward from Jordan into Syria. Gas originating from Israeli sources—in some cases swapped for Qatari liquefied natural gas (LNG) at Aqaba—is helping Syria fuel power plants and gradually restore electricity generation after years of devastating shortages.

- The recently completed Kilis-Aleppo pipeline is delivering Azerbaijani natural gas (funded by Qatar) through Turkey’s pipeline network into northern Syria, further improving energy availability.

- An improvised “pipeline on wheels” has emerged between Iraq and Syria’s Mediterranean coast. Tanker trucks reportedly transport between 140,000 and 220,000 barrels per day of crude through Iraqi Kurdistan to the Baniyas refinery and export facilities, helping bypass the Strait of Hormuz.

These projects demonstrate that Syria can play a useful role in regional energy logistics. Yet challenges arise when advocates move from practical, incremental projects toward grand strategic visions that ignore the country’s history.

Reviving the Kirkuk-Baniyas pipeline, for example, would require rebuilding hundreds of miles of infrastructure through sparsely populated terrain that remains difficult to secure. The same applies to the long-discussed Qatar-Turkey gas pipeline, plans for which Assad reportedly abandoned in 2011 under pressure from Russia. Both projects would traverse large sections of the vast desert region that stretches across central and eastern Syria and has frustrated empires—from the Ottomans to the British—for centuries. The Assad regime never fully secured it, and the current government faces even greater limitations in capacity. Protecting exposed pipeline infrastructure in these areas from sabotage would require extensive security resources, intelligence cooperation, and sustained political stability. None of those conditions currently exists.

These concerns are not limited to international projects. Proposed domestic pipelines linking Syria’s northeastern energy fields to Homs, Baniyas, and other connections would face many of the same risks.

Hard Geography

Security concerns are only part of the challenge. The larger obstacle may be economics. Much of the enthusiasm surrounding Syrian transit routes assumes that Gulf producers are eager to redirect exports toward Europe. In reality, the center of gravity for global energy demand increasingly lies in Asia. China, India, Japan, South Korea, and Southeast Asia remain the primary growth markets for Gulf oil and gas, giving producers there a strong incentive to prioritize export routes that serve Eastern markets over Western markets.

This reality strengthens the appeal of alternatives that bypass the Strait of Hormuz without crossing Syria. Saudi Arabia already possesses pipeline capacity linking Gulf production facilities to Red Sea ports, while the United Arab Emirates and Oman offer export routes to the Gulf of Oman and Arabian Sea. For most producers, these options provide access to Asian markets while avoiding many of Syria’s risks.

There are exceptions. Iraqi Kurdistan remains geographically constrained between Turkey, Iran, and Baghdad, making Mediterranean access through Syria potentially valuable. Qatar may also show renewed interest in overland routes now that the Iran war has exposed the vulnerability of LNG exports dependent on uninterrupted navigation through Hormuz. Although a Qatar-Turkey pipeline would be enormously expensive and politically complex, the strategic case for wider diversification beyond more proximal bypass routes is stronger than it was before the conflict—especially since Doha may have additional gas markets in Europe. Still, the larger regional reality remains unchanged: the principal markets for Gulf hydrocarbons lie east, not west, limiting Syria’s attractiveness as a major corridor.

Washington’s Challenge

The Trump administration and Syrian American business groups are correct to see strategic opportunity in Syria’s location. Their broader vision draws on concepts associated with the “Four Seas Initiative”—a recent proposal to link the Persian Gulf, Caspian Sea, Mediterranean Sea, and Black Sea through interconnected infrastructure networks. If realized, such projects could diversify energy transportation routes and reduce Iran’s geopolitical leverage.

Yet before investors commit billions of dollars to pipelines, Syria must become a more stable place to do business. Washington can help by reducing three categories of risk:

Political risk. The Trump administration should build on the U.S.-mediated “communication mechanism” established between Syria and Israel in Paris this January, expanding it into a broader disengagement framework along the Golan frontier. This could reduce tensions, create conditions for eventual peace negotiations, and, in the process, help ease concerns among energy investors.

Washington should also continue encouraging President Ahmed al-Sharaa’s government to broaden political participation. Alawites, Christians, Druze, Kurds, and other minorities constitute roughly a quarter of Syria’s population—including them is not simply a human rights issue, it is a stability issue. Investors are more likely to commit capital when political systems appear durable and representative.

Security risk. The United States should work with Syria, Turkey, Jordan, Iraq, Israel, and Gulf partners to improve security along prospective energy corridors. Intelligence sharing, border security cooperation, counterterrorism operations, and infrastructure protection will be essential if major pipeline projects are to move forward. Since the United States withdrew its troops from Syria two months ago, it will need to work this issue from neighboring countries. Without credible security guarantees, financing for large-scale energy infrastructure will remain difficult to obtain.

Regulatory and governance risk. Syria continues to suffer from weak institutions, opaque business practices, and pervasive corruption. Recent disputes inside the Syrian Petroleum Company between CEO Youssef Qablawi and the board—led by Energy Minister Muhammad al-Bashir—have done little to reassure investors. International energy companies require transparent contracts, predictable regulations, and enforceable legal protections before committing substantial capital. Improving governance may ultimately prove more important than constructing pipelines themselves.

Washington’s strongest remaining source of leverage in these matters is its designation of Syria as a State Sponsor of Terrorism. The Trump administration should therefore consider offering a clear, incremental path toward removing that designation if Damascus makes measurable progress on political inclusion, security cooperation, and economic reform. This approach would give Damascus a powerful incentive to act while preserving American influence over Syria’s trajectory.

In short, Washington, Damascus, and other relevant players in Syria’s energy future must bear in mind that geography alone does not create investment. Yes, Syria sits at the crossroads of multiple regions and possesses genuine potential as a future energy transportation hub. Yet for more than seventy years, pipelines crossing Syria have repeatedly fallen victim to war, political instability, regional rivalries, and sabotage. The post-Assad era presents an opportunity to change that history, but doing so will require far more than ambitious maps and optimistic projections.

If Damascus can reduce the risks that have plagued previous projects, Syria may indeed emerge as part of a broader solution to the vulnerabilities exposed by the closure of the Strait of Hormuz. If not, investors are likely to pursue safer alternatives elsewhere, leaving Syria once again watching major regional energy routes pass it by.

Andrew Tabler is the Martin J. Gross Senior Fellow at The Washington Institute. Previously, he served as senior advisor to the U.S. special envoy for Syria and director for Syria at the National Security Council.

Map Sources

Arab Gas Pipeline: EIA (2015), EIA (2025), Karam Shaar, Syria Report

Azerbaijan-Kilis-Aleppo gas route: Qatar Fund for Development, Euronews (route shown in background of inauguration ceremony), Karam Shaar, Syria Report

Kirkuk-Baniyas Oil Pipeline: Karam Shaar, Atlantic Council presentation by U.S. envoy Tom Barrack (rough route shown on slides), MEES

Qatar-Turkey Gas Pipeline: This line is theoretical, but the potential route is mentioned in various sources, including Anadolu, Hurriyet, and Karam Shaar

Pipeline on wheels: SANA, Zaman al-Wasl

Share